Regulatory uncertainty surrounding stablecoins may put conventional banks at a higher drawback than crypto corporations, stated Colin Butler, govt vp of capital markets at Mega Matrix.

Butler stated monetary establishments have already invested closely in digital asset infrastructure however are nonetheless unable to completely deploy it as lawmakers debate how stablecoins ought to be labeled. “Their basic counsel has instructed the board that they can not justify the capital funding till they know whether or not stablecoins might be handled as deposits, securities, or separate cost devices,” he instructed Cointelegraph.

A number of giant banks have already developed a few of the infrastructure wanted to assist stablecoins. JP Morgan developed the Onyx blockchain funds community, BNY Mellon launched a digital asset custody service, and Citigroup examined tokenized deposits.

“Infrastructure spending is actual, however regulatory ambiguity limits how far funding can go, as danger and compliance departments can not greenlight full implementation until they know the way the product might be labeled,” Butler argued.

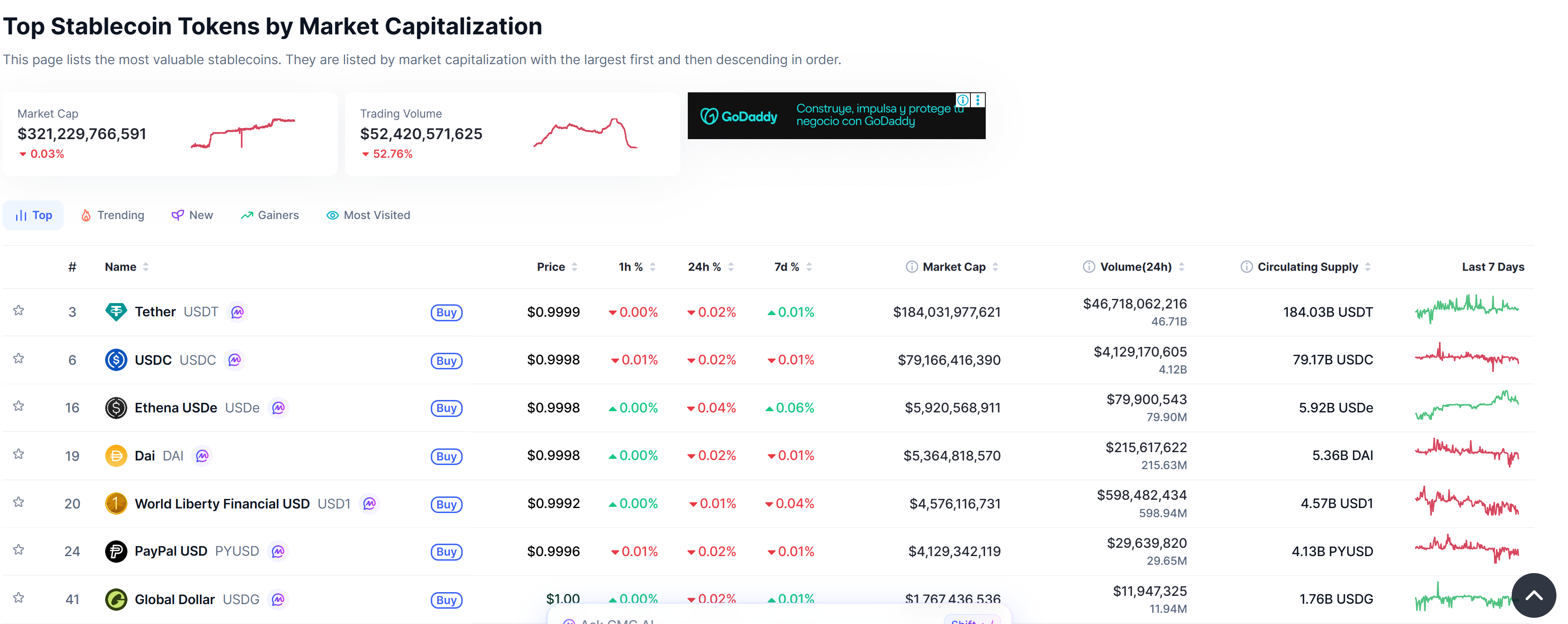

High stablecoin by market capitalization. sauce: coin market cap

Alternatively, crypto corporations which have lengthy operated in regulatory grey areas are prone to proceed doing so. “Banks, in contrast, can not function comfortably in that grey space,” he added.

Associated: USDC market cap approaches report excessive of $80 billion amid UAE ‘capital flight’: Analyst

Yield hole may trigger deposit motion

One other concern is the widening hole between the returns earned on stablecoin platforms and people earned on conventional financial institution accounts. Exchanges typically provide 4% to five% curiosity on stablecoin balances, Butler stated, however the common financial savings account within the U.S. yields lower than 0.5%.

He stated historical past exhibits savers transfer rapidly when greater yields turn out to be accessible, pointing to the transfer to cash market funds within the Nineteen Seventies. This course of may occur even quicker, because it now takes just some minutes to switch funds from a checking account to a stablecoin, and the distinction in yields is even higher.

In the meantime, Fabian Dori, chief funding officer at Sygnum, stated the aggressive hole between banks and crypto platforms is essential however not but decisive. He stated large-scale deposit flight is unlikely within the close to time period as monetary establishments proceed to prioritize belief, regulation and operational resilience.

“Nevertheless, asymmetry may speed up migration on the margins, particularly amongst enterprises, fintech customers, and globally lively clients who’re already accustomed to transferring liquidity between platforms,” Dori stated. “Aggressive pressures on financial institution deposits will turn out to be extra pronounced as stablecoins turn out to be handled as productive digital money quite than crypto buying and selling instruments,” he added.

Associated: Stablecoins may type the spine of worldwide funds inside 10 years: Billionaire

Yield restrictions could push actions abroad

Butler additionally warned that makes an attempt to restrict stablecoin yields may unintentionally steer exercise into much less regulated areas. Present US legislation prohibits stablecoin issuers from paying yield on to holders. Nevertheless, exchanges can present returns by way of lending applications, staking, or promotional rewards.

If lawmakers impose broader restrictions, capital may shift to different constructions reminiscent of artificial greenback tokens. Merchandise like Ethena’s USDe generate yield by way of the derivatives market quite than by way of conventional reserves. These mechanisms can present returns even when regulated stablecoins can not.

Butler stated if this development accelerates, regulators may face the alternative of what they supposed, as extra capital flows into opaque offshore constructions with poor shopper safety. “Capital by no means stops pursuing revenue,” he says.

journal: Bitcoin may take 7 years to improve to post-quantum — BIP-360 co-author

Leave a Reply