SEC Chairman Paul Atkins advised FOX Enterprise in December that he expects U.S. monetary markets to go on-chain “inside just a few years.” This assertion, particularly coming from the architects of Venture Crypto, the fee’s official initiative to allow tokenized market infrastructure, fell someplace between a prophecy and a coverage directive.

However what does “on-chain” imply because it applies to $67.7 trillion in public equities, $30.3 trillion in U.S. Treasuries, and $12.6 trillion in every day repo exposures? And which items can realistically transfer first?

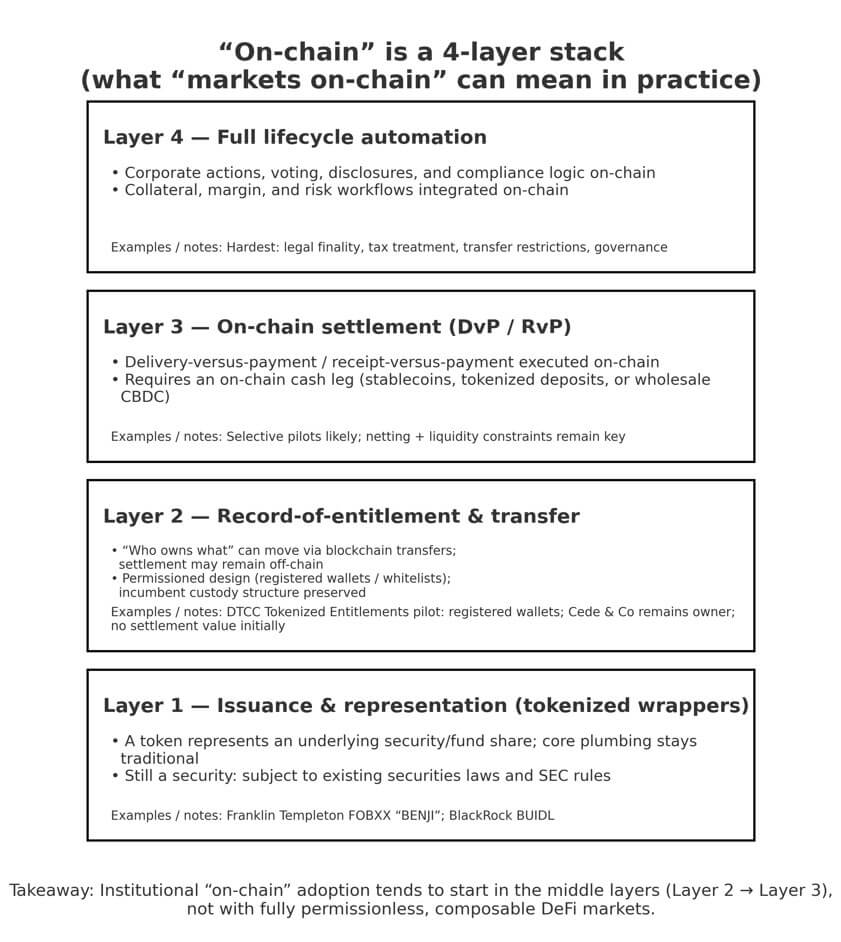

Solutions have to be correct. “On-chain” just isn’t a single factor. It is a four-layer stack, with most of what Atkins described being within the center tier and never the DeFi-native endpoints that crypto Twitter imagines.

4 flavors on-chain

Definitions are necessary as a result of the hole between tokenized wrappers and full lifecycle automation will decide what’s related in 2 years vs. 20 years.

The primary layer is publication and expression. The token replaces the underlying safety, however the plumbing stays conventional. Contemplate digitized inventory certificates. Atkins explicitly frames tokenization not as a parallel asset class, however as a wise contract representing a safety that is still topic to SEC guidelines.

The second layer is the document of entitlements and transfers. Though the “who owns what” ledger strikes by way of blockchain, funds nonetheless happen via current clearinghouses. DTCC’s Dec. 11 no-action letter from SEC Buying and selling & Markets endorses this very mannequin.

Depository Belief Firm can now subject “tokenized rights” to members by way of accepted blockchains. Nevertheless, this profit solely applies to registered wallets. Cede & Co. stays the authorized proprietor and isn’t assigned any authentic safety or settlement worth.

Translation: Tomorrow, on-chain storage and 24/7 switch can be attainable with out changing the NSCC internet.

Layer 3 requires on-chain funds with an on-chain money leg consisting of delivery-to-payment utilizing stablecoins, tokenized deposits, or wholesale central financial institution digital currencies. Atkins mentioned the theoretical potentialities of DvP and T+0, but additionally acknowledged that netting is central to clearinghouse design.

Actual-time gross settlement modifications liquidity wants, margin fashions, and intraday credit score amenities. It is tougher than a software program improve.

Layer 4 is an entire lifecycle on-chain answer protecting company actions, voting, disclosure, collateral posting, and margin calls, executed by way of good contracts. That is the ultimate state with respect to governance, authorized finality, tax remedy, and switch restrictions.

It’s also the furthest away from present SEC powers and market construction incentives.

Atkins’ two-year timeline most clearly maps to Layer 2 and Layer 3, fairly than a wholesale transition to the composable DeFi market.

Addressable universe sizing

Even when adoption begins small, the advantages can be enormous, as solely a small portion of an enormous market is big.

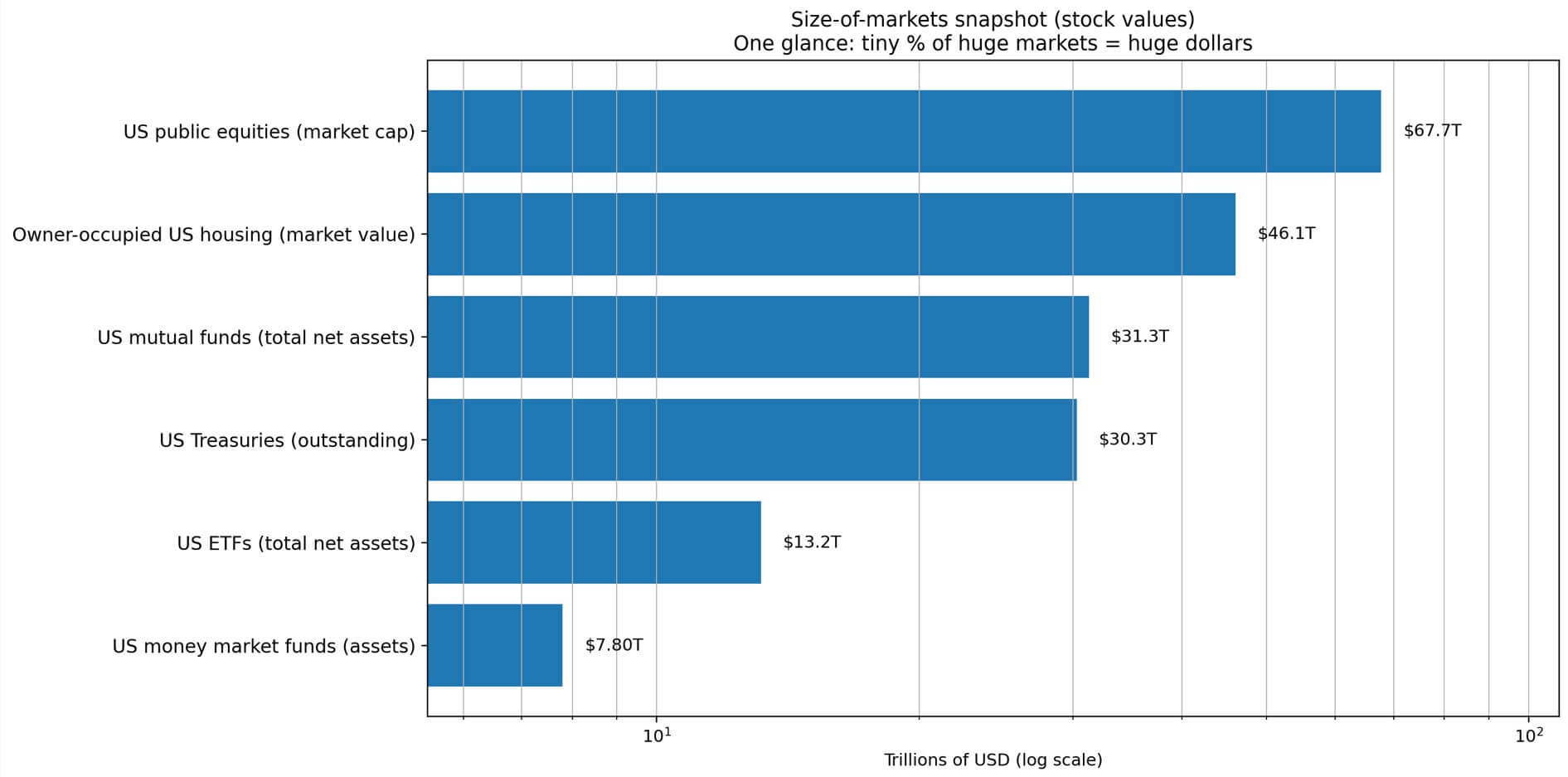

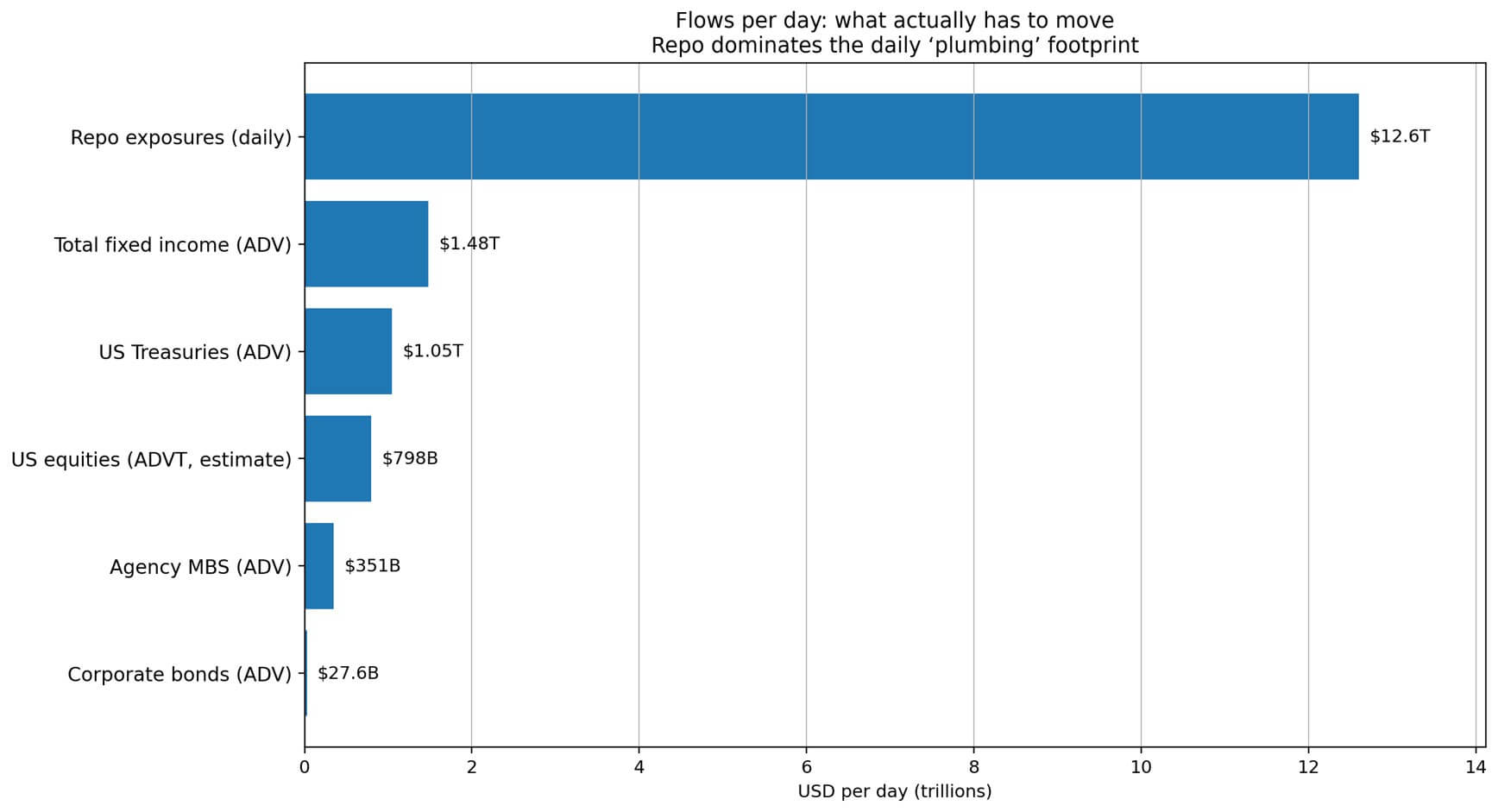

In line with SIFMA, the market capitalization of U.S. public equities was $67.7 trillion on the finish of 2025. Buying and selling density is estimated to common 17.6 billion shares per day in 2025, with common every day buying and selling worth of roughly $798 billion.

1% of inventory market capitalization is equal to $677 billion in tokenized rights. Assuming blockchain can remove the netting that presently collapses billions of transactions into a lot smaller internet debt, 0.5 p.c of every day transaction worth would signify a complete every day settlement throughput of $4 billion.

For the Ministry of Finance, the circulate is bigger. As of the third quarter of 2025, the market stability is $30.3 trillion, with a median every day buying and selling quantity of $1.47 trillion.

However the true monster is the repo. The Monetary Analysis Service estimates that common every day repo publicity can be $12.6 trillion within the third quarter of 2025, together with clearing agreements, trilateral agreements, and bilateral agreements.

If the pitch of tokenization is to cut back settlement danger and enhance collateral liquidity, repos are the place that argument turns into clear. 2% of every day repo publicity is $252 billion and will very effectively be an early wedge if establishments imagine they’ll handle and be clear.

Company credit score and securitized merchandise add one other dimension.

The whole excellent quantity of company bonds excellent is $11.5 trillion, with a median every day buying and selling quantity of $27.6 billion. Company mortgage-backed securities traded $351.2 billion per day in 2025, and non-agency MBS and asset-backed securities totaled a further $3.74 billion per day.

The whole worth of bond buying and selling will attain $1.478 trillion per day by 2025. These markets already function via custody chains and clearing infrastructure and could be streamlined via tokenization with out regulatory formalities.

Fund shares signify totally different entry factors. As of early January 2026, cash market funds had $7.8 trillion in property. Mutual funds are value $31.3 trillion and ETFs are value $13.17 trillion.

Tokenized fund shares sit within the product wrapper layer, so there isn’t any want to revamp the clearinghouse. Franklin Templeton’s FOBXX positions itself as an on-chain cash fund, and BlackRock’s BUIDL reached almost $3 billion in property final yr.

RWA.xyz tracks a complete of $9.25 billion in tokenized authorities debt, making it the highest on-chain real-world asset class.

Actual property is split into two classes. The market worth of U.S. owner-occupied houses reached $46.9 trillion within the third quarter of 2025. Nonetheless, the true world of property regulation and authorities strikes slower than software program, so county deed registers will not be tokenized at scale inside two years.

The financialized portion, consisting of REITs, mortgage securities, and securitized actual property exposures, is already within the securities pipeline and will migrate sooner.

First mover: The ladder of regulatory friction

Not all on-chain adoption will face the identical degree of resistance. The trail to minimizing friction begins with merchandise that behave like money and ends with registries embedded in native authorities administrations.

Tokenized money merchandise and short-term invoices are already occurring.

The $9.25 billion tokenized authorities bond represents significant measurement in comparison with different real-world property on-chain. As distribution expands via broker-dealer and custody channels, there’s a actual risk that it’ll develop 5x to 20x, from $40 billion to $180 billion in two years, particularly as stablecoin funds infrastructure matures.

Collateral liquidity follows carefully. Repo has $12.6 trillion in every day utilization, making it essentially the most dependable goal for the delivery-versus-payment pitch in tokenization.

Even when solely 0.5% to 2% of repo exposures had been moved to on-chain illustration, that may equate to between $63 billion and $252 billion in transactions the place tokenized collateral reduces settlement danger and operational overhead.

The subsequent step is the approved switch of rights to mainstream securities.

The DTCC pilot will authorize tokenized rights in Russell 1000 shares, U.S. Treasuries, and main index ETFs held by way of registered wallets on accepted blockchains.

If members deal with this as stability sheet and operational upgrades reminiscent of 24/7 motion, programmable switch logic, and elevated transparency, 0.1% to 1% of U.S. fairness market capitalization may turn out to be “on-chain eligible rights” inside two years. This equates to between $67.7 billion and $677 billion in tokenized claims even earlier than settlement funds are allotted.

Inventory settlement and netting redesign sit on the prime of the friction ladder. Shifting to T+0 or real-time gross settlement modifications liquidity necessities, margin calculations, and intraday credit score exposures.

Central counterparty clearing exists as a result of netting reduces the amount of money that have to be moved.

Eliminating netting means discovering new sources of intraday liquidity or accepting that gross settlement solely applies to a subset of flows.

There may be vital notional worth in non-public credit score and personal markets, estimated at $1.7 trillion to $2.28 trillion. Nevertheless, switch limitations, service complexity, and bespoke buying and selling phrases have slowed standardization.

Tokenization helps allow fractional possession and secondary liquidity, however regulatory readability concerning exemptions and custody fashions nonetheless lags.

Actual-world registries rank final. Tokenizing actual property deeds doesn’t exempt you from native recording legal guidelines or title insurance coverage necessities. Even when monetary publicity strikes on-chain via securitization, the authorized infrastructure supporting possession claims doesn’t.

Lower than the hype, better than zero

Most tokenized securities are on-chain however not publicly accessible.

DTCC’s pilot mannequin can also be permitted on public blockchains with registered wallets, permission-listed members, and institutional controls. It’s nonetheless “on-chain” within the sense of transparency and operational effectivity described by Atkins. Nevertheless, not everybody can present liquidity.

The addressable wedge in DeFi is maximized when the asset already behaves like money.

Tokenized banknotes and cash market fund shares are already collateralizing cryptocurrency market infrastructure, with BlackRock’s BUIDL being a notable instance.

The stablecoin offers a bridge layer with a provide of $308 billion and serves as an on-chain fee asset base that permits delivery-to-payment even with out a wholesale CBDC. {Dollars} went on-chain earlier than shares went on-chain.

A particular approach to measurement this: utilizing a tokenized money instrument as a beginning molecule, making use of haircuts to the switch restrictions and custody mannequin, and estimating the components that may work together with good contracts.

If tokenized US Treasuries and cash market fund merchandise attain $100 billion to $200 billion, and 20% to 50% could be posted to permissioned or semi-permissioned good contracts, which means $20 billion to $100 billion of cheap on-chain collateral.

That is sufficient of an issue for repo workflows, margin posting, and institutional DeFi.

what this really means

Atkins did not supply an in depth roadmap, however items are seen.

The SEC issued a no-action letter to the DTCC in December 2025 to pilot tokenized rights. Tokenized authorities bonds and cash market funds are increasing. A steady provide of cash offers an on-chain money layer. The repo market dwarfs shares with every day flows, and the strongest argument for tokenization danger discount is the liquidity of collateral.

The 2-year timeline doesn’t imply all securities will migrate to Ethereum. It has to do with the essential mass of the center class. That’s, second-tier rights that exist on-chain however are settled via acquainted infrastructure, and third-tier experiments the place deliveries and funds happen on-chain for particular asset courses and counterparties.

Even a 1% adoption charge throughout Treasury, cash market funds, and fairness rights would quantity to over $1 trillion in on-chain illustration.

It is not simply the US. The UK has opened a digital securities sandbox. Hong Kong has issued a HK$10 billion digital inexperienced bond. The EU’s DLT pilot scheme establishes a framework for regulated experimentation in distributed ledger issuance, buying and selling, and funds.

It is a world market and infrastructure modernization cycle, not a speculative phenomenon.

DTCC’s quarterly metrics on tokenized rights, together with complete quantity, every day transfers, registered wallets, and accepted chains, will allow you to hold observe.

The identical goes for repo transparency information from the Monetary Analysis Bureau, tokenized Treasury and cash market fund property below administration, and the availability of stablecoins as a proxy for settlement capability.

These numbers will present whether or not “on-chain inside just a few years” was a coverage or an aspiration.

Leave a Reply